Tokenized Deposits Need Interoperability

Why Cosmos and IBC Matter for Institutional Finance

The next phase of tokenized finance will not be won by issuance alone.

It will be won by connectivity.

Over the past few years, financial institutions have started exploring tokenized deposits, stablecoins, real-world assets, and blockchain-based settlement networks. The direction is clear: financial infrastructure is moving toward programmable, digital ledgers.

But a deeper question is emerging beneath the surface:

What happens if every bank builds its own tokenized money system, but those systems cannot communicate with each other?

This is the core issue behind the “cash islands” problem.

A tokenized dollar issued by Bank A may not be able to easily interact with a tokenized dollar issued by Bank B. Each institution may operate its own ledger, with its own rules, controls, compliance logic, and technical standards.

That may improve internal efficiency.

But it does not create a global financial network.

It creates isolated islands of liquidity.

And this is exactly where Cosmos and IBC become highly relevant.

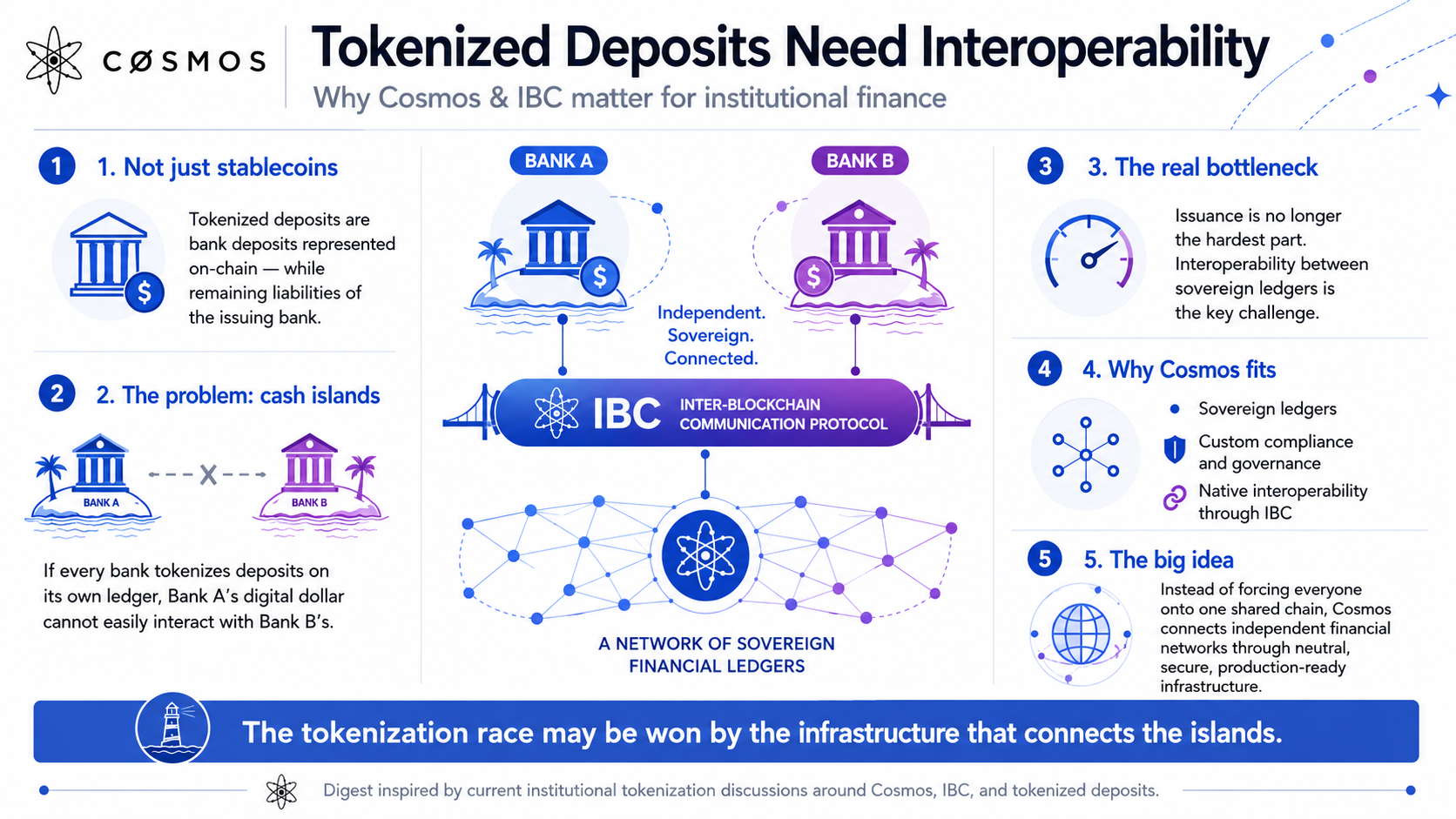

What are tokenized deposits?

A tokenized deposit is a bank deposit represented on-chain.

Unlike many stablecoins, which are issued by third-party entities, a tokenized deposit remains a liability of the issuing bank. In simple terms, the customer’s relationship with the bank stays intact, but the deposit gains the benefits of blockchain-based infrastructure.

This can enable:

- faster settlement;

- programmable payment flows;

- improved intraday liquidity management;

- better automation;

- more efficient treasury operations;

- direct integration with digital asset infrastructure.

For banks, this model is important because it modernizes the deposit without necessarily disintermediating the banking relationship.

The deposit remains inside the banking system.

The rails become programmable.

That distinction matters.

Stablecoins have captured most public attention, but tokenized bank deposits may become one of the most important building blocks of institutional on-chain finance.

The “cash island” problem

The challenge is not only whether banks can tokenize deposits.

The challenge is whether those deposits can move across different institutions and systems.

If every bank builds its own tokenized deposit infrastructure, each network may work well internally. But without interoperability, those networks remain fragmented.

Bank A can issue a digital dollar.

Bank B can issue a digital dollar.

But if Bank A’s tokenized dollar cannot easily settle with Bank B’s tokenized dollar, the financial system has not become truly connected. It has simply moved fragmentation onto new rails.

This is the “cash island” problem.

The individual islands may be advanced.

The ocean between them is still missing.

Cosmos has published similar concerns around tokenized deposit infrastructure, noting that different initiatives are emerging across different platforms with limited shared connectivity and interoperability.

Why issuance is no longer enough

In the early stages of tokenization, the main question was:

Can financial assets be issued on-chain?

Today, the answer is increasingly yes.

Banks, asset managers, payment companies, and infrastructure providers are already experimenting with or deploying blockchain-based financial systems. The harder question is no longer issuance.

The harder question is:

How do independent financial ledgers communicate securely, without forcing everyone onto a single shared platform?

This is where blockchain interoperability becomes a strategic requirement.

Without interoperability, tokenized deposits, stablecoins, tokenized funds, treasuries, and RWAs risk becoming trapped inside isolated ecosystems.

The result would be a more modern form of fragmentation.

Same walls.

New technology.

Why Cosmos is relevant to this problem

Cosmos was not designed as one monolithic blockchain where every application must live in the same environment.

Instead, Cosmos was built around the idea of sovereign, application-specific chains that can communicate with each other.

This design is highly relevant for financial institutions because banks and regulated entities often need control over:

- compliance rules;

- validator or operator sets;

- permissions;

- governance;

- transaction logic;

- privacy requirements;

- security boundaries;

- upgrade processes.

Cosmos allows teams to build custom chains while maintaining access to interoperability through IBC, the Inter-Blockchain Communication Protocol.

Cosmos documentation highlights this ability to build sovereign appchains with control over business logic, governance, permissions, and runtime configuration.

For institutional finance, that matters.

A bank may not want to become a tenant on someone else’s infrastructure. It may need to operate its own ledger, under its own rules, while still connecting to counterparties.

That is the key Cosmos thesis:

sovereignty without isolation.

IBC as connective tissue for financial ledgers

IBC is often described as a protocol for moving assets between blockchains.

But at a deeper level, IBC is a cross-chain messaging protocol.

It allows independent systems to exchange information and assets without relying on a single centralized intermediary. In the Cosmos model, each chain can remain sovereign while still participating in a broader network.

This makes IBC especially relevant for institutional use cases.

A bank could operate its own permissioned ledger.

A fund issuer could run a dedicated asset ledger.

A payment network could operate its own settlement chain.

A regulated RWA platform could maintain jurisdiction-specific compliance logic.

Instead of forcing all these systems onto one chain, IBC can provide a common communication layer between them.

Cosmos Labs describes IBC as the ecosystem’s flagship interoperability standard, with reach beyond Cosmos-native chains, including connections to environments such as Ethereum, Solana, Optimism, and Hyperledger Besu.

This is important because institutional finance will not be built on a single chain.

It will likely be built across many ledgers.

The winning infrastructure will be the one that connects them.

Sovereign ledgers fit institutional requirements

For financial institutions, infrastructure control is not optional.

Banks, payment companies, and regulated asset issuers must think about more than speed and fees. They need clear answers to operational and regulatory questions:

- Who controls the ledger?

- Who can validate transactions?

- How are keys managed?

- How are compliance rules enforced?

- Can transactions be audited?

- What happens if a counterparty system fails?

- Can the infrastructure adapt to future regulations?

This is why sovereign ledgers are so important.

A sovereign ledger allows an institution to define its own operating environment. It can choose its operators, configure permissions, implement compliance logic, and adapt the system to its internal and regulatory requirements.

Cosmos Labs positions the Cosmos Stack as a modular technology stack for building custom stablecoin, payment, tokenization, RWA, and business process automation networks, using components such as Cosmos SDK, CometBFT, Cosmos EVM, IBC, and CosmWasm.

For institutional adoption, this modularity is not just a technical feature.

It is a business requirement.

Tokenization needs more than assets

The tokenization conversation often focuses on the asset itself.

Tokenized treasuries.

Tokenized funds.

Tokenized deposits.

Tokenized real estate.

But the asset is only one part of the system.

For tokenization to scale, institutions also need:

- secure settlement;

- reliable infrastructure;

- clear compliance controls;

- interoperability between ledgers;

- connection to existing financial systems;

- auditability;

- operational monitoring;

- long-term upgradeability.

Cosmos Labs has also framed institutional tokenization as a set of infrastructure challenges: security isolation, performance, protocol-level compliance, native interoperability, and modular upgradeability.

This is where the Cosmos architecture becomes interesting.

Instead of asking all assets to live inside one shared environment, Cosmos allows different ledgers to be optimized for different use cases.

One ledger could be designed for issuance.

Another for trading.

Another for settlement.

Another for compliance-heavy institutional flows.

IBC can connect those specialized systems.

This is horizontal scaling for financial infrastructure.

Why interoperability reduces fragmentation

The financial industry has seen this pattern before.

Early payment networks often emerged in isolated environments. Over time, standardized messaging and settlement infrastructure became necessary to connect them.

Tokenized deposits may follow a similar path.

A bank-only token that moves within one internal system can create operational efficiency. But its value increases dramatically when it can interact with more counterparties, more networks, and more financial instruments.

A tokenized deposit trapped inside one network solves a local problem.

A tokenized deposit that can move across networks solves a systemic one.

That is why interoperability is not a secondary feature.

It is the foundation for network effects.

Without interoperability, every new bank, issuer, or platform adds another island.

With interoperability, every new participant expands the map.

IBC does not remove the need for regulation

It is important to be precise.

IBC can help solve the technical interoperability problem.

It does not automatically solve every legal, regulatory, or operational question.

Institutional finance still needs clear rules around:

- legal settlement finality;

- redemption rights;

- liability;

- data privacy;

- KYC and AML controls;

- sanctions screening;

- jurisdiction-specific compliance;

- risk management;

- governance between counterparties.

Technology can provide the rail.

The industry still needs the rulebook.

This is why the future of tokenized deposits will likely require both technical standards and institutional agreements.

IBC can connect ledgers.

Banks, regulators, and market infrastructure providers must define how value should move across them.

Why this matters for Cosmos

For years, Cosmos has been described as the “Internet of Blockchains.”

That phrase becomes much more concrete in the context of institutional finance.

If the future is made of many sovereign financial networks, then interoperability becomes the strategic layer.

Cosmos is not betting on one global chain absorbing every use case. It is betting on a network of specialized, sovereign systems that communicate through open standards.

That model fits the needs of institutional finance surprisingly well.

Banks want control.

Markets need connectivity.

Regulators need visibility.

Users need reliability.

Builders need modularity.

Cosmos and IBC sit directly at the intersection of those requirements.

The bigger picture: connected financial infrastructure

The tokenization race will not be won only by the first institution to issue assets on-chain.

It will be won by the infrastructure that allows those assets to move safely, reliably, and compliantly across systems.

The future of tokenized finance may not look like one giant chain.

It may look like a network of sovereign ledgers:

- each optimized for its own use case;

- each controlled by its own operators;

- each aligned with its own regulatory requirements;

- each connected through secure interoperability standards.

In that world, Cosmos and IBC offer a compelling architecture.

Not one mainland where everyone must relocate.

A network of connected islands.

Conclusion

Tokenized deposits are not just another stablecoin story.

They represent a deeper shift in how bank money could move, settle, and interact with programmable financial systems.

But without interoperability, tokenized deposits risk becoming isolated cash islands.

This is where Cosmos and IBC become strategically important.

Cosmos gives institutions a way to build sovereign ledgers.

IBC gives those ledgers a way to communicate.

Together, they point toward a future where financial networks can remain independent without becoming isolated.

The next chapter of tokenization will not only be about issuing assets.

It will be about connecting them.

And in that race, interoperability may become the most important infrastructure layer of all.

FAQ

What are tokenized deposits?

Tokenized deposits are bank deposits represented on-chain. They remain liabilities of the issuing bank while gaining the benefits of programmable ledger infrastructure.

How are tokenized deposits different from stablecoins?

A stablecoin is usually issued by a third-party issuer. A tokenized deposit represents a deposit held at a bank and remains part of the bank’s balance sheet relationship with the customer.

Why do tokenized deposits need interoperability?

Without interoperability, each bank’s tokenized deposit system may remain isolated. This creates “cash islands” where assets exist on-chain but cannot easily move between institutions.

What is IBC?

IBC, or Inter-Blockchain Communication Protocol, is a cross-chain communication protocol used in the Cosmos ecosystem to allow independent blockchains to exchange messages, data, and assets.

Why is Cosmos relevant for institutional finance?

Cosmos enables sovereign, customizable ledgers that can be adapted to specific business, compliance, and operational requirements while remaining interoperable through IBC.

Can IBC connect only Cosmos chains?

IBC started in the Cosmos ecosystem, but its scope has expanded toward broader cross-chain connectivity, including work around non-Cosmos environments such as Ethereum, Solana, Optimism, and Hyperledger Besu.

Expand Your Horizon with IBS

Stay ahead of the latest innovations in the Cosmos ecosystem and follow the progress of exciting projects by joining us on Discord and following us on Twitter.

By joining us, you are investing in a future where every interaction counts, as we build this future together, block by block. With IBS, write your own chapter in the story of true and verifiable decentralization.

Don't miss the opportunity to be part of this revolution. Join us today and help build a decentralized ecosystem for tomorrow!